Abstract

The all weather alpha portfolio has the strength of an all weather portfolio that is strong against a downtrend but overcomes the existing disadvantage of not being able to produce a return above a certain level and has an excess return greater than or equal to the market index. The LSTM model predicts the leading economic index (CLI) index, puts it into a hidden Markov model, analyzes the economic phase, and, based on this, calculates the optimal proportion of assets for each phase and invests through rebalancing according to phase transitions. Assets are made up of stocks, bonds, gold, and commodities, just like Ray Dalio's portfolio. Foreign and domestic assets are put together and allocated at a rate that maximizes the Sharpe index. Compared to Raidalio's all weather portfolio, MDD decreased by 3% in the 2020 downtrend, yields more than doubled, and the Sharpe index more than doubled. Compared to market indices and other portfolios, the Sharpe index increased by up to 9x, absolute returns increased by 4x, and MDD decreased by 3x.

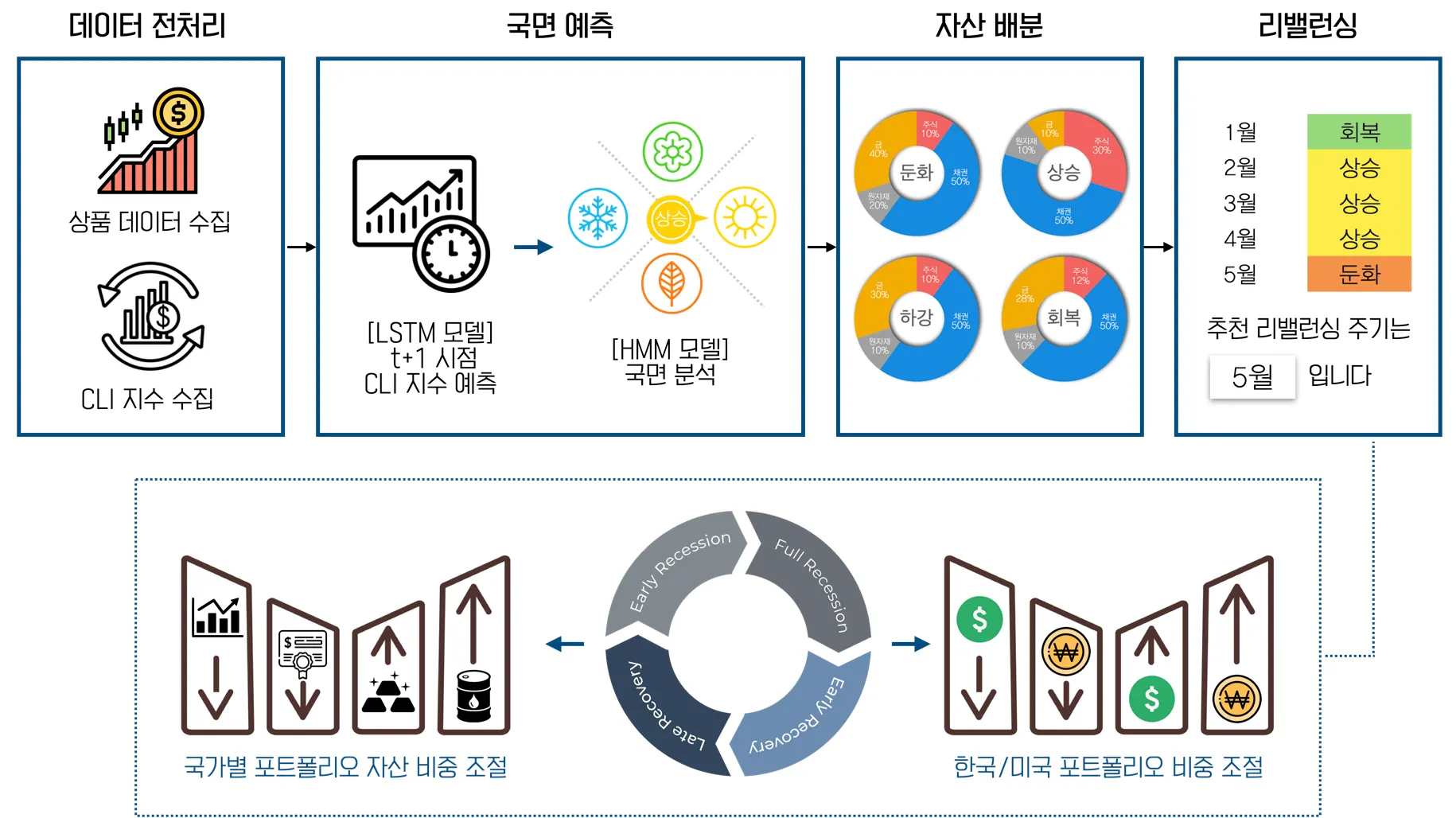

Overview of the proposed method

The All Weather Alpha portfolio consists of phase forecasting, asset allocation, and rebalancing phases. In the forecasting process, the current phase is analyzed based on CLI index forecasts. In asset allocation, the optimal asset weight is calculated for each phase. The asset weight and Korea/US portfolio ratio are adjusted for each phase at the time of transition expected through the HMM model. Rebalancing is carried out every month according to a fixed rate. Whenever a phase changes during the rebalancing process, the proportion of asset allocation is adjusted again according to each phase. Ray Dalio performed rebalancing on a one-year cycle by the fixed asset allocation. However, the All Weather Alpha Portfolio performs rebalancing by adjusting the allocation of assets according to the transition period between Korea and the United States.

Result

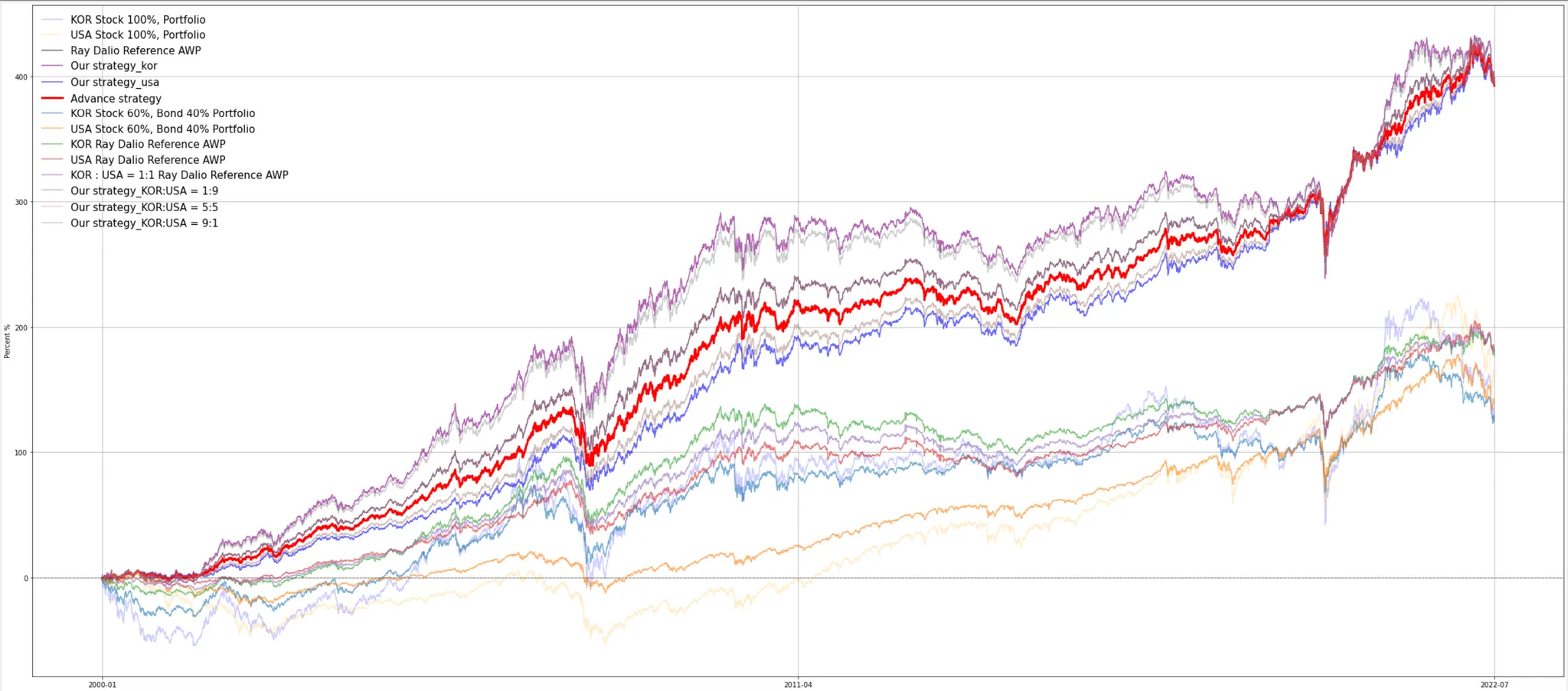

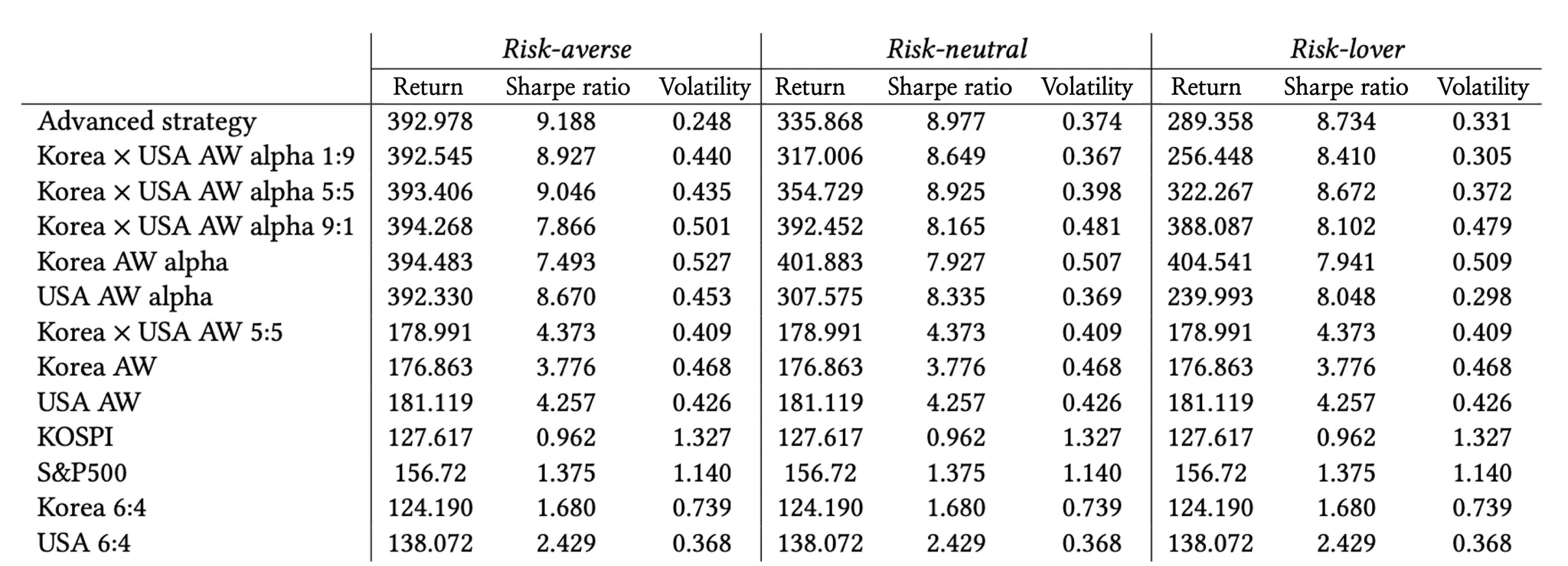

The figure shows the backtesting results for 2000-2022 of the All Weather Alpha Portfolio, which combines Korean and US assets by risk preference. The table shows the return, Sharpe index, and volatility of all portfolios used for backtesting during 2000-2022. Advanced strategy is an all weather alpha portfolio in which the weights of Korea and the US have been adjusted for each phase in the rebalancing process. Our strategy refers to the all weather alpha portfolio. We did not adjust the proportions of the Korean and US portfolios during the rebalancing process but kept them at the initially set weights. AW is Ray Dalio's all-weather portfolio. It was confirmed that the All Weather Alpha portfolio showed the best return, Sharpe index, and volatility performance. Among them, Advanced strategy recorded the highest Sharpe index. In particular, the Sharpe index of the advanced strategy in the risk-averse case shows a value of 9.188.